You’d probably think the consumer country, United States

would rank above Australia, but they are almost half of our debt per household.

Australians have a debt problem and they’re not listening.

High household debt is worrying at its best. It’s like a big semi-trailer

screaming down the highway. If something bad happens in front of it, the driver

has an extremely difficult time trying to stop, or even manoeuvre.

You’re probably saying it’s ok because our interest rates

are low. What happens when they go up a quarter of a percent or half a percent,

let alone when they creep up 1%? It’ll hurt.

The cost of

‘necessities’ like power, insurance, transport and health creep up every year.

The fastest real household spending growth (2016/17) has been in Communications

(phone, internet etc) at a rate of 6.6%, Medicine and Medical Aids at 4.9%,

Household Appliances (because we are a Nation of consumers) at 4.9%, and

Transport Services at 4.8%. Have your wages crept up at those rates?

Something has to give when household expenses are increasing

each year, and household incomes are not. It’s usually the household savings

that suffer.

So, you are in a better position than most if you actually

have savings when things change. What if you don’t?

Then your debt increases. You borrow against your home, or

you chase around for another credit card and start that evil route of spending

money you don’t have.

I don’t want to get all technical and confuse you with WPI

and GDP numbers as most of you will switch off so I’m keeping it simple.

It’s ok to have debt

if it’s manageable within your means, but just be wary that low interest

and a fairly good economy does have cycles and can change for the worst.

You need to keep a close eye on your finances, not just in

your head, or a bank’s phone APP on your account’s activity this month. No, you

really need to sit down and create a budget.

The secret is to have a plan, some guidance, direction, a

helping hand. When it comes to saving, or not spending, it’s easy enough to put

a plan in place, but whatever tool you use must break it down for you.

To take control of your money you need to understand the

flow of it: Money comes in from . . . and Money goes out to . . .

Your budgeting tool needs to show you what your finances

currently look like, what simple options are available to budget, and then how

you can easily save money from that budget.

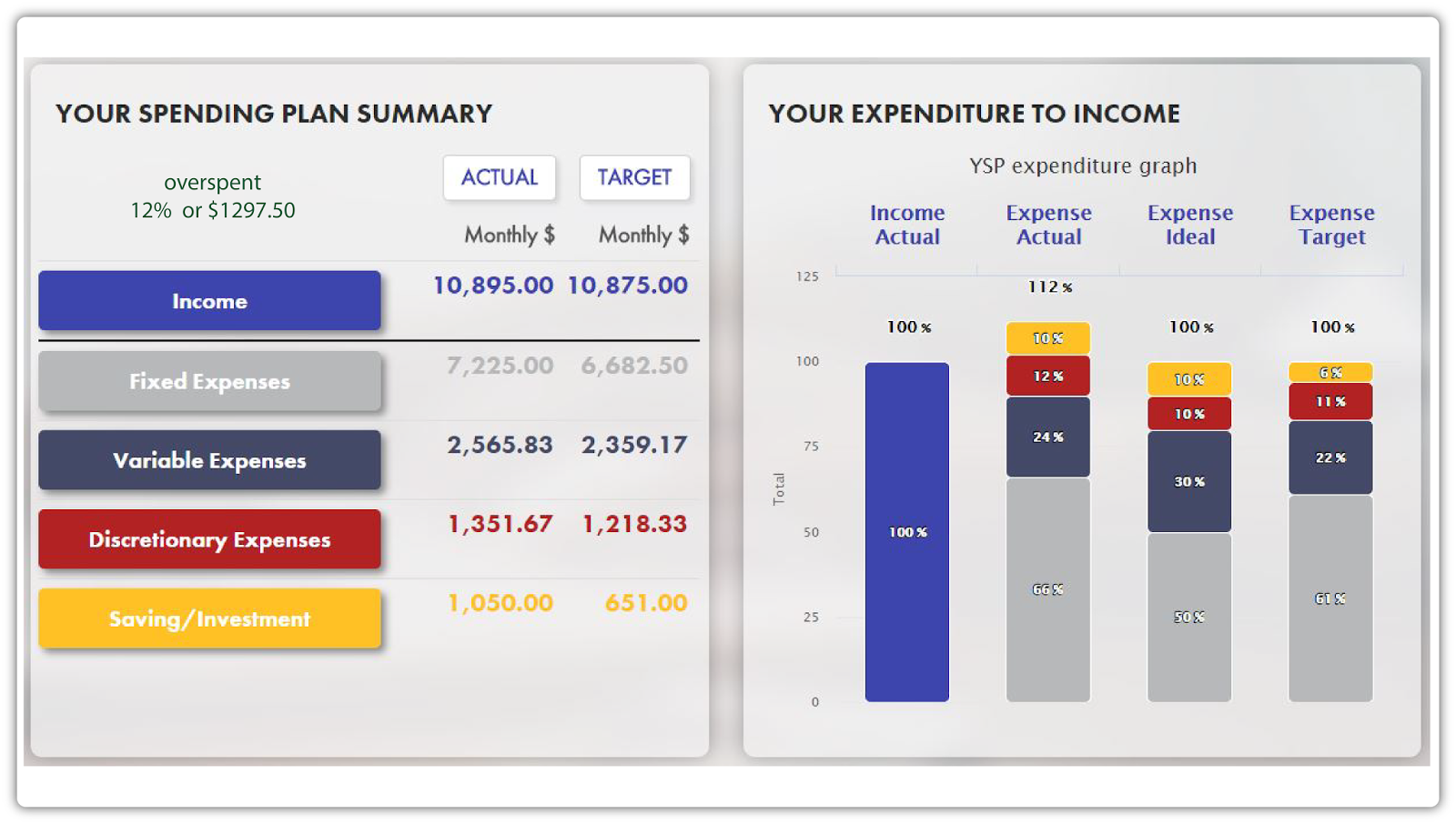

Everyone talks about a “Budget Plan”. I personally call it

“Your Spending Plan” because that is what we are trying to control here – your

spending

By creating a Spending Plan you can learn:

- ·

What your expenses are to the dollar

- ·

Know exactly what you have to spend

- ·

How to use your credit card wisely

- ·

And be able to take charge of your money and

build financial security.

If you understand how your money flows, and you can

learn that, you will see exactly what you are spending, what your expenses are,

and how small changes can save you big money.

If you’re still reading this, you obviously know that you

need something to help you manage your spending. I’m not saying to stop

spending. You just need to be able to manage your money better.

Your Wealth Vault has created a course format budget which

guides you step-by-step to create

Your

Spending Plan giving you the knowledge and capability to have optimum

control over your money.

Spending, which

you’ll still do, will take on a whole new light. You’ll be able to do it

without the guilt and remorse you currently face.

The course, and creating and managing Your Spending Plan

each month, will set you back the cost of 3 cups of coffee each month, but what

you will save on your expenses should far outweigh that cost.

If you have ANY concerns about your finances and your

spending, you need to visit

Your

Spending Plan.